Review April 2021

- Posted By David Brown

2021 continues to deliver promising economic results which look to be further supported by the various stimulus and tax cuts announced as part of last night's Federal Budget.

We’ve recently seen unemployment fall to 5.8 per cent as businesses and tourism make steady recoveries. In addition, the Reserve Bank is suggesting low interest will be the norm for some time yet. All of this has continued to strengthen property markets across many centres.

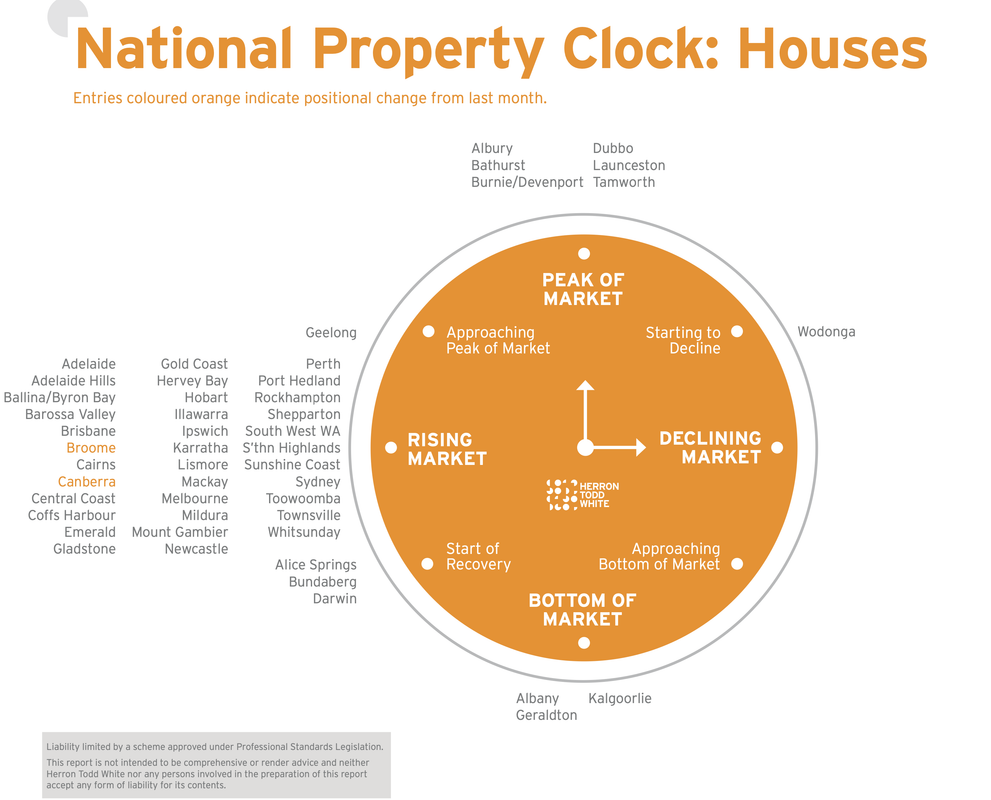

Melbourne

Australia’s property market continues to grow across the country going from strength to strength in many different locations. With owner-occupiers dominating the market, the country as a whole saw its highest number of first home buyer loan commitments since October 2009, according to the Australian Bureau of Statistics (ratecity.com.au).

The ABS reported its highest level of commitments since the government temporarily tripled the First Home Owners Grant as part of its stimulus package response to the global financial crisis. Victoria itself experienced a 19.6 per cent increase in owner-occupier loan commitments in November 2020 following the easing of COVID restrictions (ratecity.com.au).

This month we delve into which areas have seen an increase in first home buyer activity, what factors are influencing purchasing decisions as well as product types and price points that are encouraging first home buyers to enter the property market given the current economic and property climate.

Melbourne CBD

The numerous residential apartments and units within the Melbourne CBD area have generally created great interest for first home buyers, investors and renters, however, the continuing COVID-19 situation has put the CBD’s apartment market into a position of uncertainty. Without the demand created by overseas students and a lack of migration due to international border closures, the rates of vacancy throughout inner Melbourne have remained extremely high. Although these rates have improved as COVID-19 restrictions have slowly eased, they are still much higher than they were before the pandemic arriving. These high vacancy rates have also put significant downward pressure on the rental asking prices of the CBD.

With these low rental prices, first home buyers have been encouraged to continue renting rather than entering a market that has remained fairly consistent through the past months. With several grants and financial support beginning to expire, many have reverted to the option of leasing. This drop-in asking rent price is shown below, with the latest data showing an average weekly asking price of $386 for apartments – this was $600 approximately one year ago.

The drop in rent prices is contradicted by the stable performance of purchase prices in Melbourne’s CBD. The most recent statistics show that the average selling price for an apartment or unit is $483,011. This average has slowly but steadily risen in previous months and years without the major downfall that many other markets have seen.

South East

According to a recent report from the ABS, about 16,664 first home buyers were committing to a new loan in January which was the highest number since May 2009. Victoria recorded the highest number of commitments, reflecting those first home buyers in Victoria are relatively active compared to other states in Australia. As one of the hotspots for first home buyers, we are seeing an uptick in first homeowner activity in southeast Melbourne.

One of the suburbs in southeast Melbourne with strong growth of first home buyer activity is Clyde. Recent data from NAB also revealed that first home buyers lending in Clyde had grown by 32 per cent compared to the same period last year.

Clyde is located approximately 45 kilometres from the Melbourne CBD in the outer south-eastern suburban fringe and is one of the fastest-growing suburbs with a great range of nearby amenities. As of March 2021, the average asking house price in the area is $594,621. Amid the COVID pandemic, home buyers are more interested in lifestyle factors with private outdoor space and a larger living area that can accommodate a study or home office. With several government incentives such as the First Home Owners Grant and the $15,000 HomeBuilder Grant, we are seeing demand for house and land packages in the area has also increased in the past couple of months.

Inner and Outer East

Melbourne’s east has long featured some of the city’s most luxurious homes, with the price tag to match. As a result, first homeowners may struggle to enter the market in the eastern corridor, particularly in the inner east local government area of Boroondara which includes suburbs such as Hawthorn, Kew, Balwyn and Canterbury. Median house values in these suburbs sit between $2.1 million and $3.25 million (source: PropertyData. com.au 2021) and properties are unlikely to be snapped up by buyers entering the market for the first time.

There has, however, been an increase in first homeowner activity as the federal government provides financial aids and assistance in the form of grants and stamp duty discounts which help to make purchasing in the city’s leafy green east more achievable. Opportunity for buyers lies mainly in the established areas of Maroondah, Whitehorse and Knox, slightly further out from the CBD. There are not many new estates for off-the-plan purchasing of house and land packages like the northern and western corridors of the city, but there is ample opportunity for new homeowners to enter the market. Newly developed units as a result of recent subdivisions of larger lots create opportunities for more affordable property in these established suburbs.

Inner and Outer North

Record low interest rates and several government incentives have resulted in an enormous amount of activity from first home buyers in Victoria since the beginning of the year. On top of this, the Coronavirus pandemic resulting in the inability to go on holidays meant many who were still working were able to spend their savings on the property instead. Since the announcement of the Homebuilder scheme, the value of lending to first home buyers has increased by 86.8 per cent (source: ABS, 2021). Melbourne’s inner and outer north is no exception to the first home buyer boom seen across the rest of Victoria. One of the clear hotspot suburbs in Melbourne’s outer north for first home buyers is Kalkallo, which currently boasts an affordable median house price of $547,450 (source: PropertyData, 2021).

The west presents as a more accessible area for first home buyers compared to other parts of Melbourne. First homeowner activity has definitely increased in the west with government incentives being an important factor in purchasers’ decision making. The first home buyers grant includes $10,000 for those who buy or build their first home with the stamp duty tax being waived from the purchase. The grant is $20,000 for those who decide to build in regional Victoria. This is combined with the new Home Builders grant which is $25,000 for build contracts signed before 31 December 2020 and $15,000 for contracts signed before 31 March 2021 (source: realestate.com.au). These incentives have driven the occupancy market in areas such as Tarneit, Truganina and the Melton region from renting to owning or purchasing. Extremely low interest rates are also a driving force for first home buyers purchasing a property.

The average price for property in March 2021 in Tarneit, Melton and Williamstown was $570,000, $391,250 and $1.4 million respectively. Clearly, there is a huge difference in price points from the established inner and bayside areas of the west compared to the developing areas. Areas such as Tarneit and Melton give purchasers options as they can purchase an existing property or build, meaning they can take full advantage of government incentives in an area they can actually afford. Areas such as Williamstown are out of reach for most first-time buyers.

Areas in the Wyndham Vale and Melton municipalities have been more desirable and will continue to be for first home buyers because of: their relative proximity and linkages to the city; the more desirable property type and size, being larger parcels of land and dwelling areas; and most importantly they are affordable and realistic for the large majority of first home buyers.

Geelong

Geelong, much like the rest of Victoria has seen an uptick in first homeowner activity to start 2021. Subsidy programs and stimulus packages such as HomeBuilder and JobKeeper, along with low-interest rates and a ban on international travel have meant more people are in a position to purchase a home despite the trying times.

First-time buyers have been drawn to more affordable locations including Lara, Leopold, Charlemont and Armstrong Creek where buyers can enter the market at around the $550,000 price point for a four-bedroom home. Popular suburb Armstrong Creek will continue to be attractive for first-time homeowners. With a median house price of $575,000, this area will continue to be one of Geelong’s most in-demand growth markets (source: Corelogic, 2021).

Fringe suburbs of Bell Post Hill and Grovedale offer affordable properties on larger allotments within proximity to major infrastructure and have proven to be popular options with first-time buyers and young families targeting these locations.

Brisbane

It’s been a very active first three months of 2021 in the Brisbane market as we’ve watched the rate of sales activity increase at a fast clip.

All the usual universal factors are fuelling the buzz – low-interest rates, government stimulus and rising confidence that post-pandemic normality is just around the corner. These are the same drivers applicable across most Australian property markets at present.

But in Brisbane, we have one particular unfair advantage over other eastern-seaboard capitals

– and that’s affordability relative to proximity. We’ve got a property at a very accessible price level that’s still within a short commute of our CBD (or CBDs if you count satellite centres such as Ipswich and Logan). This means people priced out of southern-state real estate are looking here to make their mark.

A big part of the demographic buyer base helping drive demand in Brisbane has been first home buyers. Activity among first-time buyers has strengthened for some reasons.

Firstly, government stimulus has been geared toward first homebuyers through programmes such as:

- Early access to superannuation for a deposit;

- Queensland Transfer Duty on homes valued under $550,000 can save buyers up to $15,925;

- Queensland First Homeowners Grant of $15,000 towards buying or building a new home; and

- The Federal Homebuilder grant provided $25,000 for contracts signed between 4 June and 31 December 2020 and $15,000 for contracts signed between 1 January and 31 March 2021.

In addition, the rental market in Brisbane has been very hot indeed. Combine this with extraordinarily low-interest rates on borrowing and the result is that it actually makes more economic sense to buy a home than to rent. Not only are you getting a foot on the property ladder, but it’s cheaper servicing a mortgage than paying a landlord.

Of course, all of this is occurring at a time of growing confidence. With the vaccine rollout underway and some impressive results from countries such as the UK in terms of falling infection rates, there is a feeling that we’re emerging from the pandemic.

But for all these advantages, we do note that the Brisbane market has ratcheted up again in recent weeks and could be getting away from many first-home buyers prices. Tight stock levels and strong demand across all demographics have made it incredibly difficult not only to find a property to buy but to also secure something at a reasonable price. Investors have made their way back into the market and competition is heating up.

So, what is actually available to first home buyers in our city if they have the cash and are ready to go?

Well, first-timers are most active in the sub -$500,000 price sector for detached houses (even though finding a property at this level is becoming very tough). Most house buying at this price point is in the far northern and southern fringe suburbs.

As such, there has been increased interest in attached housing from first homebuyers – both units and townhouses. This compromise helps keep their purchase options affordable while still being able to buy in areas that are well serviced and accessible.

In fact, for those wishing to purchase closer to the CBD and/or transport hubs, units are the most obvious choice. For example, new or near-new units in Nundah are available within the $320,000 to $450,000 price bracket.

Another market to keep an eye on is Ipswich. This LGA has seen impressive sale results of late, but you can still buy a well located three-bedroom home for under $600,000. Take this property at 16 Murphy Street, Ipswich which sold in April 2021 for $570,000. It’s on a particularly small allotment – just 367 square metres – but offers a three-bedroom home in a well-elevated position with exceptional views to the north and within walking distance of Ipswich’s CBD.

Sunshine Coast

The residential market on the Sunshine Coast over the past 24 months has seen a significant improvement in sales volumes and values. The pace of these increases in some cases has been breathtaking. This had made it harder for first home buyers to enter the market but mainly

for traditional properties. Generally, the first home buyer market on the Sunshine Coast is predominantly the $300,000 to $600,000 value range, however as a result of the low stock levels and increase in values across the coast, opportunities in this price range are becoming harder to secure.

This has led to developers and builders getting creative with lot sizes and the design of new homes to provide more affordable housing options. Developers and builders have a variety of lot sizes and house designs targeting first home buyers from small-lot detached housing (sub-250 square metre lots) to terrace style housing (circa 100 square metre lots) that provide small two- to three-bedroom, two-bathroom accommodation with a single lock-up garage. Some first homeowners are now turning to these smaller house options in order to get a foot in the door as an alternative to strata-titled townhouses and units. These product types have become more common in the two master-planned estates of Aura and Harmony.

The traditional 600 square metre lot with a four-bedroom, two-bathroom dwelling with a double lock-up garage is becoming a lot harder for first homeowners to obtain, especially in coastal areas. However, if you move further from the coast to the hinterland towns, your options can open up significantly. Older post-war dwellings, townhouses and duplexes all come into play. For instance, in Nambour near the hospital, you can still buy an older partly renovated home on a 916 square metre allotment in the high $300,000 range. A late 1990s townhouse in that same area is in the low $300,000 range. Sure, they are not shiny and new, but they do provide an option for first home buyers to enter the market.

In the coastal locations, clearly the values tick up, so it is harder. The unit market has been the main focus here with older townhouses and smaller walk-up units providing options.

The big issue for first homeowners is the level of competition in the market which is magnified at these lower price points. On the back of the tight rental markets, investors are looking for opportunities.

There are a number of strategies being used to enter the market. These range from utilising the First Home Owners Grants on offer, to using their parents’ equity as guarantor for a home loan and avoiding having to pay mortgage insurance. The current low-interest-rate environment is also providing significant assistance with the difference between paying rent and a mortgage being minimal.